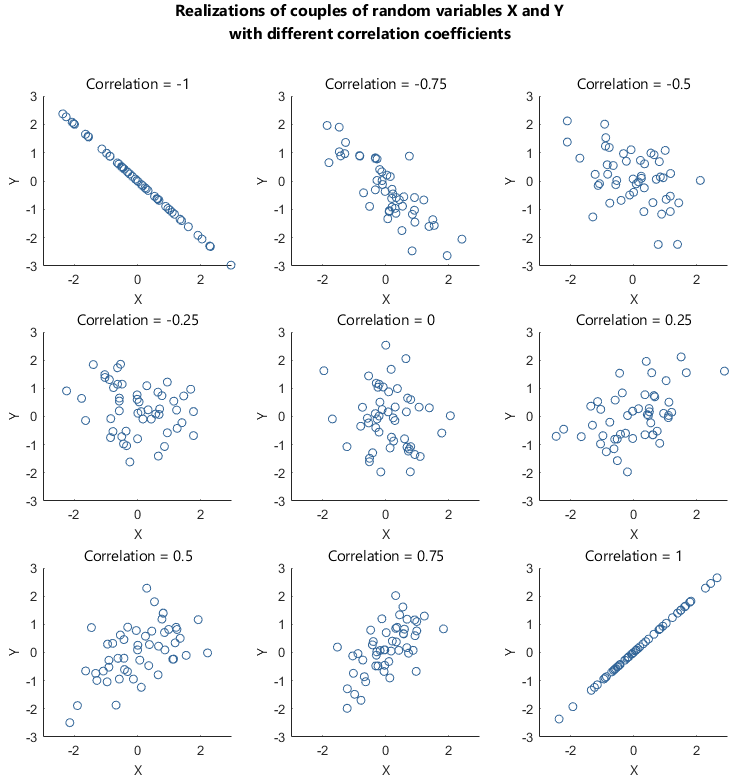

Computes a “normalized covariance” between two variables by taking into account their standard deviation. Cor(X,Y)=σXσYCov(X,Y) probability